OnPoint Subscriber Exclusive

The Big Picture brings together a range of PS commentaries to give readers a comprehensive understanding of topics in the news – and the deeper issues driving the news. The Big Question features concise contributor analysis and predictions on timely topics.

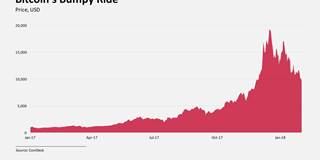

The Rise and Fall of Bitcoin?

Bitcoin investors’ fortunes have soared and plummeted in recent months. But how concerned about the economic role and impact of cryptocurrencies should the rest of us be?

Featured in this Big Picture

https://prosyn.org/woW7PJx;